Q2 FY25 Highlights at a Glance

- Net profit: ₹433 crore, up ~15 year-on-year.

- Net premium income: ₹16,570 crore, a rise of about 12 %.

- Total income: ₹28,583 crore, up 5.8 % sequentially.

- Operating profit: down 11.8 % YoY because of higher expenses and GST adjustments on older policies.

- Value of new business (VNB): ₹938 crore, up 17 % YoY.

- VNB margin: 24.3 %, compared with 26.3 % a year ago.

These numbers show that while premium growth remains solid, profitability is under strain. The company is still expanding its reach, but each new policy now adds slightly less profit than before.

Breaking Down the Performance

1. Premium Growth and Product Mix

HDFC Life saw strong traction in both new policies and renewals. Bancassurance and digital sales channels did well, contributing to consistent inflows. However, the mix of business shifted toward lower-margin savings and ULIP products. That mix helped revenue but compressed overall margins.

2. Operating Profit Pressure

The fall in operating profit stems mainly from two issues:

- Regulatory and tax changes, particularly the GST treatment of older policies, created one-time costs that cut into earnings.

- Rising expenses, distribution commissions, employee costs, and technology spending outpaced income growth.

Because life-insurance profit margins are slim, even moderate cost increases have a visible impact on results.

3. VNB and Profitability Trend

VNB measures the present value of expected future profits from new policies. Although VNB grew in rupee terms, its margin narrowed to 24.3 %. This means the company is selling more business but earning slightly less on each new policy. It highlights the need for a higher share of protection and annuity products, which carry better margins.

4. Investment Income and Market Conditions

Investment income remained steady, supported by stable bond yields. However, mild equity-market volatility and mark-to-market adjustments capped returns. As insurers invest large sums in fixed-income securities, a change of even 0.5 % in yields can affect reported profits.

5. Expense Ratio and Efficiency

Operating costs rose faster than total income. The expense ratio, the share of costs in total premium income, increased slightly. Management will need to tighten spending to restore profitability momentum in the upcoming quarters.

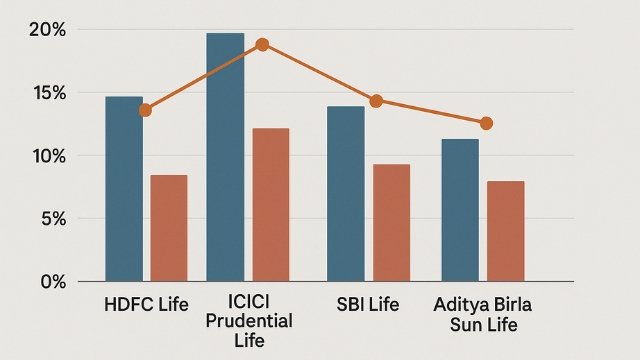

Comparing HDFC Life with Peers

In India’s private-sector insurance space, competition remains strong:

- ICICI Prudential Life: Reported ~19 % YoY profit growth, with better cost control and product balance.

- SBI Life: Continues to lead on scale and consistent margin performance.

- Aditya Birla Sun Life: Smaller base but improving cost ratios and steady double-digit growth.

HDFC Life’s strength lies in its brand and long track record, but its current growth is average compared with peers. The stock trades at a valuation premium, which leaves little room for disappointment.

Sector and Macro Context

India’s insurance penetration (life plus non-life) is about 4 % of GDP, below global averages. Rising financial literacy, digital adoption, and government incentives are expected to push this higher over the next few years. According to IRDAI data, total life-insurance premiums in India grew roughly 13 % YoY in FY24. HDFC Life captures around 7 – 8 % of the market, giving it solid scale but room to grow further.

At the same time, policy reforms and new taxation rules can affect product demand. The FY24 change, removing exemptions for high-premium traditional policies, for example, shifted demand toward protection and annuity products. Companies that adapt fastest to such changes gain a lasting advantage.

Risks to Consider

- High expenses: Rising distribution and technology costs may keep margins under pressure.

- Regulatory risk: Frequent policy changes on insurance taxation or product limits can alter growth assumptions.

- Market volatility: Equity and bond swings affect investment income and reported profits.

- Valuation risk: At 80–85× earnings, any growth miss can lead to a quick stock correction.

- Product mix imbalance: Too much focus on ULIPs or low-margin savings plans limits profitability potential.

Opportunities and Growth Drivers

- Insurance penetration remains low; the long-term growth opportunity is significant.

- A shift toward protection and annuity plans can lift VNB margins by 200–300 basis points.

- Digital platforms and data-based underwriting can reduce acquisition costs.

- Partnerships with banks and fintechs expand reach with limited fixed overheads.

- Improved yield environment in fixed income could boost investment returns.

Valuation Scenarios

Based on current market levels and analyst estimates:

| Scenario | Fair P/E Range | Implied Price Target (₹) |

|---|---|---|

| Optimistic (growth > 15 % | 80–90× | 800–900 + |

| Base (growth ~ 12 % | 65–70× | 650–750 |

| Conservative (flat growth) | 50–60× | 500–650 |

The stock’s current valuation already prices in strong execution. If profit growth stalls, it could drift toward the base range.

Investment Outlook: Buy, Hold, or Sell?

- For new investors: Wait for clearer signs of margin recovery or a better entry price. The upside from here looks limited unless growth surprises positively.

- For existing holders: Holding makes sense. HDFC Life remains financially solid, with stable solvency ratios and a trusted brand. Keep monitoring quarterly margin trends.

- For cautious investors: You can reduce exposure or diversify into other financial stocks until consistent growth resumes.

Overall, a Hold stance is balanced. The business remains strong, but the stock already reflects optimistic expectations.

Monitoring Checklist for Q3–Q4 FY25

- VNB margin and product-mix improvement.

- Operating expense ratio movement.

- Investment income yield and mark-to-market adjustments.

- Any regulatory updates from IRDAI or GST Council?

- Peer comparison in profit and margin growth.

Call to Action: For deeper insight, you can request our comparative dashboard covering HDFC Life, SBI Life, and ICICI Prudential, complete with valuation metrics and growth trends.

Frequently Asked Questions About HDFC Life Q2 Results Analysis

Q1. What explains the rise in profit despite margin pressure?

Answer: Profit rose mainly because premium income expanded faster than expected. Even with slightly weaker margins, higher sales volume pushed total profit up. One-time GST adjustments capped the gain, but the base business remains strong.

Q2. How serious is the drop in VNB margin?

Answer: The drop from 26 % to 24 % is notable but not alarming. It reflects a change in product mix rather than structural weakness. If the company increases its share of high-margin protection plans, the margin can return to prior levels within a few quarters.

Q3. How do valuation levels compare with global peers?

Answer: At around 80× earnings, HDFC Life trades richer than most Asian life-insurance peers, which average 30–40×. The premium reflects investor faith in India’s growth story and the brand’s stability, but it also raises risk if growth slows.

Q4. What are analysts saying?

Answer: Brokerage opinions are mixed. Some maintain a “Buy” citing long-term demand, while others rate it “Hold” due to limited near-term upside. The consensus target price clusters between ₹700 and ₹780, roughly 5–10 % below current highs.

Q5. How could interest-rate moves impact results?

Answer: Higher yields help new investments earn more, but they can also lower the market value of older bonds. Overall, moderate rate increases are positive for long-term income, though short-term volatility can affect quarterly results.

Q6. Are there any structural strengths supporting HDFC Life?

Answer: Yes. The company has strong solvency ratios (above 200 %), diversified distribution channels, and one of the widest product portfolios in the sector. Its brand reputation and customer trust give it resilience in slower cycles.

Q7. What should investors focus on in upcoming results?

Answer: Key points: growth in new business premium, stability of expense ratio, and signs of VNB margin improvement. If these metrics improve while valuation stays stable, sentiment toward the stock will likely strengthen again.

HDFC Life is a legacy name in India’s insurance sector, and the Q2 results reflect both strength and stress. Its premium momentum remains strong, but margin pressure and regulatory costs raise concerns. The stock’s valuation assumes performance will improve; if that fails, downside risk may be steep. But for now, holding is fair for many investors, with selective entry possible post-correction or once a clear margin turnaround appears.

Disclaimer:

This article is meant solely for educational and informational purposes. It is not intended to be financial, investment, insurance, or trading advice. The analysis of HDFC Life’s Q2 FY25 results is based on publicly available information at the time of writing, and company performance, regulations, and market conditions may change over time. We are not registered with SEBI, RBI, or IRDAI as investment or financial advisors. Always conduct your own research and consult a certified financial professional before making decisions related to buying, holding, or selling any insurance or financial-sector stock.