In today’s uncertain world, one of the foremost concerns for a parent is: “Will my child’s dreams be secured even if I’m not around?” Whether it’s higher education, overseas studies, entrepreneurial ventures, or starting life on their own terms, crafting the right financial base early makes all the difference. In this comprehensive guide, we delve into how child-specific life insurance plans function, what features to look for, how they compare to other investment options, the latest developments (2025-26), and how to choose the right plan in India. Our aim: this will be your one-stop, go-to article on the subject.

1. Why Child-Insurance Plans Matter

When you begin saving for your child’s future, you typically think of mutual funds, PPF, real estate, bank FDs, or stocks. But there’s a key risk: you must be alive to continue investing, manage them, and have timely access to the corpus when required. That is where child-insurance plans step in, offering both investment/savings and life cover together.

What Makes Them Important?

- Dual Benefit: These plans offer protection (life cover for the parent) and savings/investment for the child’s future.

- Waiver of Premium: In the eventuality of the parent’s demise (or disability, depending on the plan), future premiums are waived, but the policy continues, ensuring the child’s corpus builds uninterrupted.

- Milestone Planning: The payout is structured to align with key child milestones (e.g., 18–21 years of education / 25 years of marriage/career launch).

- Tax Efficiency: Premiums can qualify under Section 80C (up to ₹1.5 lakh in many cases), and maturity proceeds are often exempt under Section 10(10D).

- Peace of Mind: The greatest mental relief for a parent is knowing the child’s future won’t be jeopardised because of the parent’s absence or incapacity.

The Reality of Rising Costs

- Education and career costs are escalating. According to insurers, the cost of education in India is rising at ~11-12% annually.

- If you delay starting, you lose precious years of compounding and security cover.

Hence: Start early, select smartly, and pick a policy aligned with your child’s goals.

2. What Are Child-Insurance Plans & How Do They Work

Understanding the mechanics is crucial before you buy. Let’s break it into digestible parts.

2.1 Types of Child Plans

As per recent research and guidance:

| Type | Description |

| Child Education Plans | Designed primarily for funding a child’s education (higher studies, abroad, etc.). Combines savings + cover. |

| Child ULIP Plans (Unit-Linked Insurance Plans) | A portion of the premium goes into investment in funds (equity/debt) + life cover. Higher returns potential, higher risk. |

| Child Savings/Endowment Plans | Traditional plans: savings portion grows in debt or guaranteed instruments; survival benefits or lump payouts. Lower risk. |

2.2 How They Work

1. Entry & Premium Payment

- You, as parent (or proposer), pay premiums for a defined premium payment term, e.g., 10, 12, 15 years or regular until the child reaches a certain age.

- Entry age: parents’ age (usually 18-55) and child age (often from birth or up to say 12/15).

2. Life Cover & Waiver of Premium

- The plan provides life cover for the proposer. If the proposer dies (or becomes totally permanently disabled, depending on the plan), the insurer waives future premiums and possibly pays a death benefit immediately. The policy continues building.

3. Investment/Savings Component

- The premium allocated to savings grows over the tenure. In ULIPs, it is market-linked; in traditional ones, it may be guaranteed or based on bonuses.

4. Payout(s)

- On maturity (when the child reaches a predetermined age or policy term ends), the corpus is paid out as a lump sum, as instalments, or a mixture, depending on the plan. Some money-back plans give periodic payouts along the way.

- Death benefit: In the event of a parent’s demise during the policy term, the child (or nominee) gets the sum assured immediately (or as per the plan) plus future premiums waived.

5. Tax Benefits

- Premiums eligible for deduction under Section 80C (within limit) and maturity/death benefits are often tax-free under Section 10(10D).

2.3 Example in Real Life

Say you want to accumulate ₹20 lakh for your child’s higher education when he/she turn 21. You start a child plan at birth, pay annual premiums for 15 years, with a maturity term aligning with age 21. You select sum assured + savings component. If you (the parent) die when the child is 10, the future premiums are waived, but the policy keeps building towards maturity. On maturity, the ₹20 lakh (or more, depending on returns) is paid to your child, thus fulfilling the goal even if you were not there.

3. Key Features You Must Evaluate

When you’re shopping for a child plan, focus on the following features: they make the difference between a good plan and a mediocre one.

3.1 Waiver of Premium Benefit

If the parent (proposer/insured) dies or becomes totally and permanently disabled, the plan must continue without you paying further premiums. This is one of the most critical features. Many plans include it; some let you add it as a rider. Bajaj Life Insurance+1

3.2 Flexible Premium Payment Term

Check how long you need to pay premiums. Some allow limited pay (e.g., pay for only 10 or 12 years), others regular pay until the child reaches 21/25. Flexibility here is valuable.

3.3 Choice of Policy Term & Payout Age

Make sure the maturity/payout age aligns with your child’s goal, e.g., age 18 (college), age 23 (post-graduation), age 30 (marriage/business). Some plans allow partial payouts at milestones (like age 18, 21) and a final payout at age 25.

3.4 Investment Option / Returns

If it’s a ULIP, evaluate: fund options (equity/debt/hybrid), switching facility, and transparency of charges. For traditional plans: check guaranteed additions, bonuses, and earlier money-back features. E.g.: a traditional money-back child plan in Life Insurance Corporation of India (LIC) offers periodic payouts. Liferay DXP+1

3.5 Partial Withdrawals / Liquidity

Some plans permit partial withdrawals after lock-in (often 5 years) for mid-term needs (e.g., sibling’s education, starting a business). If you need flexibility, favour plans with this option.

3.6 Tax Efficiency & Cost Structure

Check:

- Premiums are eligible for 80C.

- Maturity/death benefit tax-free under 10(10D) (subject to conditions).

- What are the charges (fund management, mortality charges, premium allocation), especially in ULIPs?

- Check the claim settlement ratio and the reputation of the insurer.

3.7 Payout Options & Customisation

Does the plan allow you to choose: lump sum vs instalments? Do you get the option for partial withdrawals? What riders are available (critical illness, accidental death, career start bonus)?

3.8 Early Start Advantage & Compounding

Starting early (say, child age 0–5) means a longer horizon for savings, more time to ride out volatility (if ULIP), and more time for compounding. An insurer emphasises this: “starting early allows better returns, flexibility, time to evaluate policy features”.

3.9 Inflation Factor

Education/marriage costs will inflate significantly. Choose a sum assured that factors in inflation, and preferably a plan where the savings grow based on market returns or bonuses. An article notes: “makes you stay ahead of inflation”.

4. Advantages & Limitations

Advantages

- Security for your child: Even if you are no more, the plan continues, and the benefits go to your child.

- Discipline in savings: Regular premiums create a savings habit and ensure the corpus builds steadily.

- Peace of mind: Knowing the future is safeguarded frees you to focus on other aspects of life.

- Tax benefits: As discussed, valid deductions and tax-free proceeds.

- Flexible goals: Education, overseas studies, marriage, business start-ups, can all be targeted.

- Combined solution: One plan serves both protection and savings – instead of separate term insurance + mutual funds.

Limitations / Things to Watch

- Returns may be modest, especially in traditional plans where growth is guaranteed but limited. If you want higher returns, you must take ULIP risks.

- Charges in ULIPs can be higher; if you discontinue early, returns may suffer.

- Liquidity is low: You cannot easily stop paying or withdraw early without loss; surrender charges may apply.

- Not a substitute for pure term insurance: If your priority is only protection, pure term cover may serve you better. Child plan adds savings but at the cost of a higher premium vs pure term.

- Sum assured may be insufficient if delayed: If you start late (say when the child is already 10 or 12), you may need to pay a high premium or accept a lower corpus.

- Mis-match of payout age: If the policy ends at age 18, but your child wants to study till 22 or do an MBA, you may face a shortfall.

5. Latest Trends & 2025-26 Updates

Let’s look at what’s happening in India for child insurance/education plans in the current landscape.

- Many insurers now offer multi-milestone payouts, e.g., at age 18, 21, and 25, instead of a single maturity lump sum.

- A shift towards ULIP-based child plans with more fund options (more equity allocation) to potentially beat inflation. For example, an article lists the best child insurance policies in June 2025, including ULIPs from HDFC Life, ICICI Prudential, and Bajaj Allianz.

- Emphasis on waiver of premium on disability as well as death.

- Insurers are providing more online onboarding, and flexible premium payment frequency (annual, half-yearly, monthly) and policy terms.

- Growing awareness of combining a child plan with other tools, e.g., you may still allocate part of your savings to PPF, mutual funds, etc. An article on child investment plans lists PPF, Sukanya Samriddhi, equity mutual funds, along with child insurance.

- Enhanced transparency on charges, better fund switching in ULIPs.

- From a regulatory viewpoint, the broad life insurance sector is under pressure to keep plans simpler and more consumer-friendly, though for child plans the features remain many.

- On taxation & broader ecosystem: there are announcements of GST reduction or exemption on life insurance premiums (to make protection more affordable), which may indirectly benefit child plans.

6. Child Plans vs Other Investment Alternatives

How do these child insurance plans compare with other popular instruments you may consider for your child’s future?

| Option | What it Offers | Main Advantages | Main Disadvantages | Best When |

| Child Life Insurance Plan (Savings + Cover) | Combines life cover (for parent) + savings corpus for child | Security + savings in one plan; waiver of premium; tax benefits | May cost more than plain savings; returns may be moderate; less liquidity | You want both protection & savings for your child’s future |

| Term Insurance + Separate Savings/Investment | Pure term cover for parent + you separately invest in mutual funds/PPF, etc. | Cheapest cover + full control of savings/investment | Requires discipline and separate management; no automatic linkage between cover & savings | You are comfortable managing separate instruments and want maximum savings return |

| Pure Investment Plans (PPF, SIP in Mutual Funds, SSY for Daughter) | Focus purely on savings/investment for the child’s future | Potential higher returns (mutual funds), tax-efficient (PPF/SSY) | No death cover; risk of incomplete corpus if parent dies early; separate risk management needed | You already have sufficient life cover and want aggressive savings |

| Traditional Endowment / Money-Back Plan (without child focus) | Savings + cover, but not purpose-aligned with child milestones | Safe and familiar | May not align with child costs and may lack flexibility & waiver benefits | If you prefer very low risk and modest goals |

Key takeaway: If the primary goal is to protect the child’s future and not rely solely on your earnest efforts, a child-insurance plan performs both roles. If you already have adequate protection and are comfortable with managing savings/investments, you may pick other instruments.

7. How to Choose the Right Child Plan – Step by Step

Here is a practical roadmap to follow:

Step 1: Estimate the corpus needed

- Ask: What will this cost when my child reaches the goal age (e.g., 18–22 years)? Consider inflation (say, education inflation ~ 10% per annum).

- Use online calculators or speak to an advisor. Some child plan product pages allow an estimate of maturity benefit at 4%/8% growth.

Step 2: Entry-age & horizon

- The earlier you start (child’s age 0–5), the better. If the child is already older (say 10–15), you may need a higher premium or shorter tenure.

- Choose a payout age that matches your target: college, postgraduate, marriage, or business start.

Step 3: Premium Payment Term

- Choose whether you want to pay for a limited years (e.g., 10–12 years) or till a later date. Limited pay = higher yearly premium but shorter burden.

- Check for premium payment flexibility (monthly/half-yearly/annual).

Step 4: Choose the type of plan

- If you are comfortable with market risk and want higher returns, the ULIP variant.

- If you prefer guaranteed or less-risky savings, a traditional/savings child plan.

- Always compare features, fund options, and transparency of charges (for ULIPs).

Step 5: Check features

- Waiver of premium (ensure it’s included).

- Death benefit/ sum assured on the mortality of the parent.

- Partial withdrawals or early payouts (if needed).

- Bonus or loyalty additions (in traditional plans).

- Fund switching facility (in ULIPs).

- Payout option: lump sum/instalments/mixture.

- Riders: Critical illness, accidental death, disability, and family income benefit.

- Tax benefit eligibility.

- Claim settlement ratio of the insurer.

Step 6: Compare cost vs benefit

- Look at the sample illustration: premium vs maturity benefit vs sum assured vs what happens on death. Many insurers publish brochures.

- Be wary of very high charges or mediocre fund performance.

Step 7: Read the fine print

- What happens if you skip a premium? What is surrender value? What are lock-in conditions (ULIP usually 5 years)?

- Are withdrawals allowed? What is the charge?

- What happens if the parent changes job/country, or the child’s study plan changes?

- How are bonuses/loyalty additions declared in traditional plans?

Step 8: Review periodically

- Life events: job change, additional child, change in goal timeline, revisit the plan.

- In ULIP, monitor fund performance, switch if necessary.

- Keep track of policy documentation, nominee details, and policy servicing online.

8. Comparative Table: Top Child Plans in India (2025 Snapshot)

Below is a simplified comparison of some of the popular child plans in India (please treat these as indicative – always refer to official brochures).

| Insurer & Plan | Type | Entry Age (Parent–Child) | Notable Features | Good For |

| SBI Life Insurance – Smart Scholar Plus | ULIP Child Plan | Parent: 18–57 yrs, Child: 0–17 yrs | Investment with multiple funds, waiver of premium, loyalty additions | Growth-oriented parents who can take market risk |

| Max Life Insurance – Future Genius / Child Saving Plan | Traditional Child Saving Plan | Parent: 21–45 yrs | Guaranteed money-back during graduation, flexible premium payment | Conservative savers seeking guaranteed outcomes |

| Bajaj Allianz Life Insurance – Young Assure | Child Saving Plan | Parent: 18–50 yrs | Guaranteed additions, special rates for female policyholders, and multiple installment payout options | Balanced savers wanting partial payouts |

| ICICI Prudential Life Insurance – Smart Kid Plan | ULIP Child Plan | Parent: 20–54 yrs | Market-linked returns, fund options, life cover for child goals | Parents are comfortable with the ULIP investment component |

| Tata AIA Life Insurance – Child Education Plan | Traditional Child Plan | Varies | Combined savings + cover, flexible payout options (lump/instalments) | Parents who prioritise simplicity and known corpus |

Note: The table is for illustration only. The actual sum assured, premium, term options, minimum entry age, fund options, and charges will differ. Always obtain and study the latest product brochure before purchase.

9. Estimated Premium Table (Indicative)

Below is a sample table of what premiums might look like for typical child plans – these are hypothetical and for illustration only; actual premiums vary significantly by insurer, plan variant, sum assured, term, and age.

| Child’s Age | Parents Age at Entry | Policy Term (Years) | Annual Premium Approx. (₹) | Corpus Target (₹) |

| 0 yrs | 30 yrs | 18 yrs – child age 18 | ~ ₹ 60,000 | ~ ₹ 20 lakh |

| 0 yrs | 35 yrs | 21 yrs | ~ ₹ 70,000 | ~ ₹ 25 lakh |

| 5 yrs | 30 yrs | 13 years | ~ ₹ 85,000 | ~ ₹ 20 lakh |

| 10 yrs | 35 yrs | 11 years | ~ ₹ 1,20,000 | ~ ₹ 20 lakh |

Again: these numbers are for illustration. Always calculate based on your plan’s terms and assumptions of growth (say 4% conservative, 8% optimistic) and inflation. Many insurers publish tables: e.g., Parent age 18, Child age 0, policy term X years – maturity corpus will be Y at 4%/8%.

10. Frequently Asked Questions About Child-Focused Life Insurance Plans

Q1. When should I buy a child plan?

Answer: Ideally, as early as possible, even froma child’s birth or early years. The earlier you start, the lower your premiums for a given corpus, and the more time your savings have to grow. If you delay, you may either pay high premiums or compromise on the corpus.

Q2. What if the child’s goals change (for example, wants overseas studies instead of India)?

Answer: Yes, you should re-evaluate. If you have a ULIP-based plan, you may switch funds, increase premium (if allowed), or top up. If you have a traditional plan, review your premium or consider additional savings/investments.

Q3. Can I stop paying premiums later?

Answer: You can in the event of a parent’s death or disability (waiver of premium feature) if built in. Otherwise, if you stop paying prematurely, the policy may lapse or the surrender value may be very low. Always check the surrender conditions and impact on the corpus.

Q4. Do these plans also cover a child’s death?

Answer: Primarily, the cover is on the parent/proposer. Some plans may have child cover as a rider, but the core idea is: protect the child’s future if the parent is lost. If a child dies, typically the death benefit may go to the parent or nominee, but that is not the main goal of the plan.

Q5. How do these plans perform compared to keeping money apart (say in SIPs or PPF)?

Answer: It depends. If you have separate term insurance (for protection) and you invest aggressively in mutual funds (for savings), you may earn higher returns (especially if you invest in equity for the long term). However, the advantage of child plans is their built-in protection + savings combined, and the psychological assurance. If you are disciplined and proficient in investing, you may pick separate instruments. Otherwise, the child plan is a simpler, integrated solution.

Q6. Tax implications?

Answer: Yes. Premiums may qualify under Section 80C (within ₹1.5 lakh limit) if the plan is eligible. Maturity/death benefits often exempt from tax under Section 10(10D), subject to conditions. Always confirm with the latest tax laws. ICICI Prudential Life Insurance

11. Real-world Checklist Before You Buy

- Compare at least 3–5 child plan options (ULIPs and traditional). Use comparison sites like PolicyBazaar, which list “Best Child Insurance Plans in India 2025”.

- Read the product brochure thoroughly (sum assured, benefit table, exclusions, riders, charges).

- Ensure waiver of premium is inbuilt, not optional at extra cost (or check its cost).

- Confirm maturity/payout age aligns with your child’s goals (college, marriage, business).

- Check the insurer’s claim settlement ratio and reputation (this indicates the likelihood of smooth benefit payout).

- Understand charges (for ULIPs especially): premium allocation, fund management, mortality, switching charges, lock-in period.

- Confirm the flexibility: premium payment term, ability to increase premiums, fund switching, and partial withdrawal.

- Gauge your risk appetite: if you want high returns and are okay with volatility → ULIP; if you want safety and predictability → traditional.

- Factor in inflation: aim for a corpus higher than the current cost of education/marriage.

- Keep policy documents, update the nominee, keep track of bank account details for payout, and ensure KYC is done.

- Review annually: Are premiums affordable? Has your target corpus changed? Do you need to top up or switch funds?

12. Common Mistakes to Avoid

- Starting too late (child is already 12-15 years) and expecting a huge corpus with a small premium.

- Choosing a plan solely for the lowest premium or maximum return without checking features (waiver, payout age, flexibility).

- Underestimating inflation or the cost of overseas education.

- Ignoring liquidity, if you need funds earlier, a child plan might restrict you.

- Treating the plan as “set and forget”, you should review periodically.

- Ignoring separate protection: some parents assume the child plan replaces term insurance; it doesn’t provide large protection cover like a pure term plan.

- Paying a premium from borrowed money or not making sure you can continue payments, discontinuity kills benefits.

- Not reading the fine print, e.g., what happens if the parent becomes non‐resident, or if the child goes abroad.

13. Making the Most of It: Tips for Parents

- Start early and pay regularly; small amounts now build a big corpus later.

- Align the payout milestone with the child’s choice: If the child is more likely to study till age 24 or start a business at age 25, make the term accordingly.

- Use the policy as part of a diversified savings strategy; you might still invest in SIPs, PPF, or SSY alongside.

- Engage the child: Teach them about savings and security; let them understand a part of the plan so they value it.

- If you change jobs/career/relocate abroad, ensure premiums can continue and the policy doesn’t get compromised.

- Monitor funds (if ULIP) and switch if required, but not in panic over short-term market fluctuations; the horizon is long-term.

- Use the policy to lock in disciplined saving, rather than occasional large lumps.

- Ensure that the bank account & nominee details are always updated so benefit payout is smooth when needed.

- Keep copies of premium receipts, bonus/loyalty additions statements, and fund value statements (ULIP) – helps during claim.

- Factor in inflation and rising costs: reassess every 2-3 years whether the corpus target needs revision.

14. Final Thoughts

For a parent, there’s no greater comfort than knowing the child’s future is secure even in your absence. Child-focused life-insurance plans provide a meaningful combination of protection + savings to make this possible. Starting early, selecting suitable features, and matching the payout age to your child’s goals are critical. While these plans are not perfect (they may have moderate returns, less liquidity than pure savings), their integration of protection and planning, which are meant to guard the dreams, not just accumulate money, sets them apart.

If you ask: “Will the child’s future be financially secure if I’m no longer around?” – then yes, with the right child plan, you can say yes, confidently.

Appendix: Sample Premium Table & Comparison Table

A. Sample Premium Table (Indicative)

(As above in Section 9)

B. Comparison Table of Some Top Plans

(As above in Section 8)

Sample Premium Illustrations (2025)

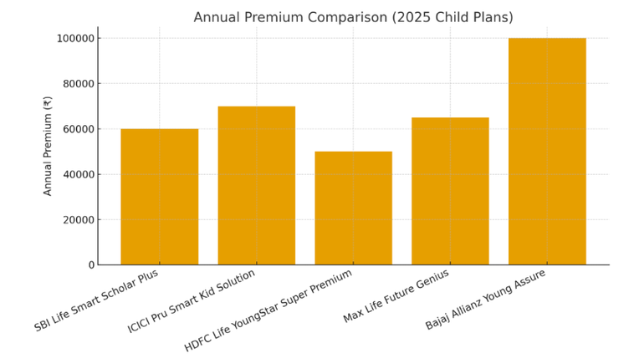

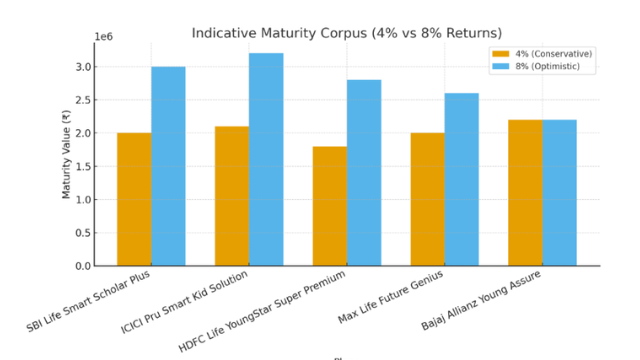

| # | Insurer & Plan | Plan Type | Entry Age (Parent / Child) | Assumed Annual Premium | Term (Premium Pay / Benefit Term) | Indicative Corpus/Benefit at Maturity* |

| 1 | SBI Life Insurance – Smart Scholar Plus | ULIP (child plan) | Parent ~30 yrs / Child – newborn | ₹ 60,000/yr | Pay for ~15 yrs → Benefit at child age ~21 | ₹ 20-30 lakh (assuming 4%-8% returns) |

| 2 | ICICI Prudential Life Insurance – Smart Kid Solution | ULIP (child plan) | Parent ~35 yrs / Child ~2 yrs | ₹ 70,000/yr | Pay 12 yrs → Benefit at child age ~20 | ₹ 21-32 lakh (4%-8% return band) |

| 3 | HDFC Life Insurance – YoungStar Super Premium | ULIP (child plan) | Parent ~30 yrs / Child ~0 yrs | ~₹ 50,000/yr | Pay for ~14 yrs → Benefit at ~age 18-22 | ~₹ 18-28 lakh (4%-8% assumed) |

| 4 | Max Life Insurance – Future Genius Child Saving Plan | Traditional Child Saving Plan | Parent ~30 yrs / Child ~1 yr | ₹ 65,000/yr | Pay for ~15 yrs → Benefits at key milestones (education/marriage) | Variable, with guaranteed/money-back style payouts |

| 5 | Bajaj Allianz Life Insurance – Young Assure | Endowment / Child Saving Plan | Parent ~32 yrs / Child ~0 yrs | ₹ 1,00,000/yr | Pay 10-15 yrs → Benefit at maturity around child age ~20 | ~₹ 22 lakh (based on 1 lakh/yr illustration) |

Important: The “Indicative Corpus/Benefit” assumes hypothetical growth rates: e.g., 4% (conservative) to 8% (optimistic) for ULIP style. Traditional plans may have guaranteed additions + bonuses which differ. For actual values, consult official plan illustrations.

What to Note When Comparing

- The entry age of parent and child matters: younger child + younger parent means longer horizon, lower premium for the same target.

- ULIP-type plans expose your savings to market risk; hence, the “4%-8% return band” used here. Traditional plans offer more predictable but often lower growth.

- The “Term” column above includes: how many years you pay premiums & till when the benefit is expected (often child age 18-25).

- Premium amounts I’ve shown are annual for illustration only; many plans also allow monthly/half-yearly modes.

- Benefit amounts are not guaranteed (especially for ULIPs) and will depend on actual performance, charges, policy lapse, etc.

- The percentages (4%–8%) are assumed purely for illustration and may not reflect actual fund returns or bonuses.

How to Use This Table

- Pick 2-3 plans you are interested in.

- For each plan: get the official premium illustration from the insurer (which will show the premium schedule, benefit table, death benefit, waiver of premium, and maturity payout).

- Using your child’s current age and your target (e.g., college at 20, overseas education at 23), plug in premiums and terms that match your goal.

- Compare across plans: cost (premium) vs benefit (maturity + death benefits).

- Factor in risk appetite: If you are okay with market swings → ULIP; if you want guaranteed outcomes → traditional saving plan.

Disclaimer:

The above charts, figures, and comparisons are purely for illustration and educational purposes. We are not registered with SEBI (Securities and Exchange Board of India) as investment or financial advisors. The data presented does not constitute financial advice, recommendation, or solicitation to buy or sell any insurance or investment product. Readers are advised to consult a qualified financial advisor or the respective insurer before making any investment or purchase decisions. Actual plan features, premiums, and returns may vary based on insurer terms, product variants, and market conditions.