HDFC Bank, one of India’s largest private sector banks, released its financial results for FY 2024-25 in April 2025. Alongside profit & loss disclosures, the bank published its consolidated and standalone balance sheets and key ratios. As of March 31, 2025, HDFC Bank’s total balance sheet size stood at ₹ 39,102 billion (i.e., ₹ 39,102,000 crore) on a standalone basis. For comparison, a year earlier (March 31, 2024), the size was about ₹ 36,176 billion.

Because HDFC Bank merged with its parent HDFC (Housing Development Finance Corporation) on July 1, 2023, some of the historical comparatives need to be interpreted carefully; there is a change in scale, asset mix, and funding structure. With that caveat, one can still draw meaningful insights from the latest balance sheet trends, ratio analysis, and banking metrics.

Balance Sheet Snapshot: Scale & Structure

At the core, a bank’s balance sheet shows how it raises funds (liabilities + equity) and how it uses them (assets). The FY 25 numbers show HDFC Bank is running a large and complex balance sheet with aggressive growth ambitions.

According to the Q4 FY 25 presentation, on a standalone basis:

- Average deposits for the quarter were ₹ 25,280 billion, up ~15.8% year-on-year

- End-of-period deposits (March 31, 2025) were ₹ 27,147 billion, up ~14.1% from prior year

- Advances under management averaged ₹ 26,955 billion (up ~7.3% YoY)

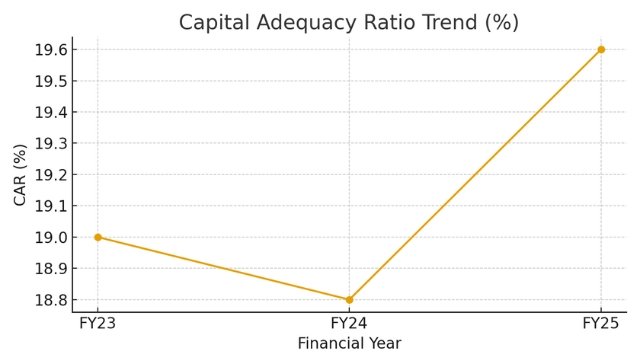

- Net profit for the quarter was ₹ 176 billion, delivering a return on assets of ~1.94% and a capital adequacy ratio of 19.6% (CET1 ~17.2%)

- Gross non-performing assets (GNPA) stood at 1.33% (ex-agri 1.13%)

- Cost-to-income ratio was ~39.8%, and net interest margins (excluding tax refund interest) were ~3.46% on total assets

- For consolidated operations, the bank’s net revenue and bottom line reflected the combined operations, including subsidiaries and merged entities.

Because I don’t have the complete audited asset side line-by-line here, I rely on these key aggregates and publicly available trends. The Moneycontrol balance sheet page offers more granular breakdowns (e.g. equity, investments, borrowings), which confirm that shareholder funds, borrowings, and other liabilities also play a nontrivial role in the funding mix.

What stands out is the sheer size, the reliance on deposits, and the relatively concentrated exposure in advances. The bank is pushing scaling hard.

Funding Side: Deposits, Borrowings, Equity

Deposits remain by far the primary source of funds. The ~14–16% growth in average deposits and end-period deposits is healthy, especially for a large bank starting from a large base. That kind of growth suggests strong traction in core banking relationships and customer confidence. The growth was not only year-on-year but also quarter-on-quarter (QoQ), indicating consistent inflows.

Within deposits, CASA (current + savings) is always a key metric because it typically offers lower-cost funding. In Q4 FY 25, CASA grew: average CASA rose QoQ by ₹ 0.11 trillion, and end-period CASA rose ~8.2% QoQ. Time deposits (term deposits) also increased, but at a slightly higher cost.

However, despite this strong growth, the deposit base is under pressure because the loan book has grown rapidly, pushing the bank’s loan-to-deposit ratio (LDR) to a high level (discussed later). To sustain further growth without stress, deposit momentum must be preserved or strengthened.

Borrowings and other non-deposit liabilities also matter, especially when deposit growth lags or when liquidity stress arises. In the post-merger entity, borrowings have increased to fill gaps. While deposits dominate, borrowings cannot be ignored.

Equity and retained reserves provide stability. The bank’s capital adequacy (19.6%) is comfortably above regulatory minima. The fact that the bank maintains a strong buffer is positive. Equity growth must keep pace with asset growth to prevent leverage from becoming excessive.

One caveat: raising equity is more expensive and dilutive, so the bank must balance growth ambitions with capital discipline. If deposit growth falls behind, incremental growth might force reliance on borrowings or equity, which can squeeze returns.

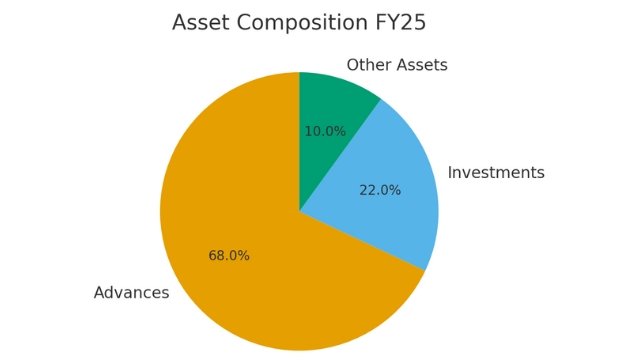

Asset Side: Advances, Investments & Liquidity Deployment

On the assets side, the biggest line is advances: loans to corporates, SMEs, retail, mortgages, etc. With the merger, the loan portfolio expanded deeply, and HDFC Bank is aggressively deploying capital into advances.

In Q4 FY 25, average advances were ~₹ 26,955 billion (7.3% YoY growth). The end-period advances growth was ~7.7% YoY. Some segments (retail mortgages, personal loans, auto) have shown steady incremental growth.

This suggests the bank is trying to balance between leveraging its legacy home-finance strength and scaling in consumer, small business, and corporate lending. The diversification helps reduce concentration risk.

The investment portfolio (government securities, bonds, etc.) plays multiple roles: it provides liquidity, interest income, and cushions against depositor redemptions. HDFC Bank has increased its securities holdings, reflecting prudent liquidity buffer planning.

Cash and balances with the central bank, and balances with banks (call money/short notice) are smaller but critical for liquidity. The bank cannot allow this buffer to shrink too much, especially when it is running a high LDR. Any mismatch or sudden outflow can stress operations.

In summary, the bank is putting large sums into earning assets (advances), while still holding investment and liquidity buffers. The risk is: if interest rates move unfavorably or credit cycles deteriorate, those buffers will be tested.

Ratio Analysis & Performance Metrics

To truly understand the balance sheet, one must examine key ratios:

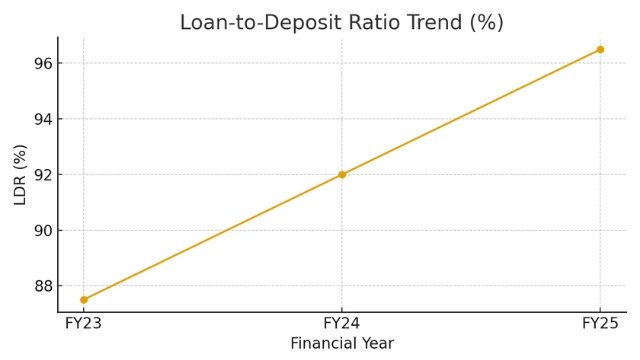

1. Loan-to-Deposit Ratio (LDR)

This measures how much of the deposits are turned into loans. A very high LDR suggests aggressive lending, leaving less room for liquidity cushions. HDFC Bank’s LDR is estimated at ~96.5%, which is high for a bank of its size. In fact, the bank itself has stated its intent to bring this down to around 85–90% over the coming years.

Such a high LDR leaves less slack, and during stress periods, deposit outflows or slower deposit growth can bite.

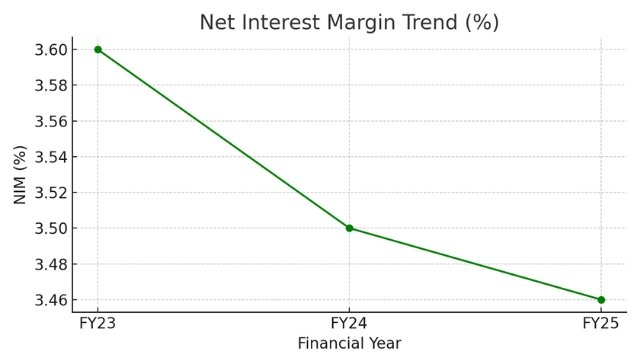

2. Net Interest Margin (NIM)

This is the spread between interest earned and interest paid, divided by interest-earning assets (or total assets). In Q4 FY 25, excluding interest from tax refunds, NIM was ~3.46% on total assets. On interest-earning assets, the effective margin was slightly higher (~3.65%) in some disclosures.

Given the competitive lending environment and funding cost pressures, maintaining margins in the 3.4–3.6% range is decent. The question is whether the bank can sustain it in a rising interest rate cycle or when deposit costs rise.

3. Cost-to-Income Ratio

This ratio reflects operational efficiency. A lower number is better (less cost to generate each rupee of income). HDFC Bank clocked ~39.8% in Q4 FY 25. In banking, that is quite respectable, especially for a large institution.

It suggests strong cost control, scale benefits, and efficiency in operations. However, sustaining or improving it while growing aggressively will require continuous innovation and process discipline.

4. Asset Quality: GNPA, Net NPA, Provision Coverage

Gross NPA stood at 1.33% in Q4 FY 25; excluding agriculture, it was ~1.13%. That level is acceptable for a large bank in India, but not low enough to be comfortable.

Loan growth always brings a risk of slippages. The bank must maintain adequate provisions and constantly monitor sectoral stress. The fact that NPAs are not ballooning despite rapid growth is a plus, but external shocks (e.g., realty stress, commodity cycles) could test this.

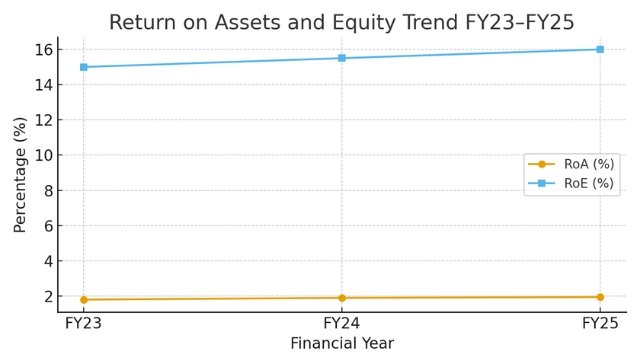

5. Return on Assets (RoA) and Return on Equity (RoE)

In Q4 FY 25, the standalone RoA was ~1.94%. On equity, with a strong capital base, RoE in double digits remains possible (depending on leverage and provisioning).

But RoE is sensitive: if provisions rise, or margins compress, returns will suffer. The bank must manage growth, risk, and costs in tandem.

Strengths: What HDFC Bank Has Going For It

There are several points of strength visible in the numbers and trends.

First, the bank commands a strong deposit franchise. Growth in deposits has not lagged despite its large size. That speaks of customer trust, brand power, and operational reach. CASA growth adds ballast. If the bank can tilt the mix more toward low-cost deposits, that will further strengthen it.

Second, it is deploying capital aggressively. The bank is not sitting on idle reserves; it is pushing money into advances and investments to generate yield. That reflects confidence in the lending environment and a growth posture.

Third, efficiency is a plus. Keeping cost-to-income under 40%, especially while scaling, shows operational competence. Many large banks struggle with scale inefficiencies; HDFC Bank appears to manage that reasonably.

Fourth, capital buffers are comfortable. A CRAR of ~19.6% gives headroom for expansion and cushions against shocks. The CET1 ratio (~17.2%) shows that core equity is solid. These buffers help during downturns.

Fifth, margin firming and interest spread management appear sustainable, though not immune to external stress. The bank’s discipline in balancing asset yields and cost of funds has held margins within a healthy band.

Finally, asset quality has not deteriorated dramatically despite growth. The moderate GNPA, along with stable provisioning, suggests underwriting discipline has been respected.

Risks & Red Flags: What Could Go Wrong

No analysis is complete without flagging what could go sideways.

The most immediate risk is the very high LDR (~96.5%). This leaves little breathing space between loans and deposit funding. Any slowdown in deposit growth or sudden deposit withdrawals could stress liquidity, forcing reliance on borrowings or asset sales.

Credit risk is ever-present. Rapid loan growth can mask latent stress, especially in sectors susceptible to cycles (real estate, construction, infrastructure, commodity-linked industries). If macro conditions worsen, some loans may slip, and provisioning needs might surge.

Margin compression is another risk. If funding costs (especially deposit costs) rise faster than loan yields, NIM will be squeezed. In a rising interest rate environment, this has to be managed carefully via hedging, ALM (asset-liability management), and selective pricing power.

Liquidity risk emerges when buffers are thin. If the bank over-allocates to advances and under-invests in liquid assets, sudden demands (e.g. large withdrawals, surprises) might cause stress.

Integration risk is relevant given the HDFC merger. Systems, processes, culture, risk models, all need alignment. Any misstep in integration can cause inefficiencies, internal friction, or execution errors.

Capital may become a constraint. If growth continues at a high clip, maintaining capital adequacy might force fresh equity issuance or slower growth. New equity could dilute returns, so the bank must calibrate its expansion plans carefully.

Finally, external shocks, macro slowdown, regulatory tightening, regulation changes, interest rate volatility, or unforeseen events (pandemic, geopolitical), can stress any bank. HDFC Bank must remain vigilant and maintain buffers.

Strategic Implications & What to Watch

Given the strengths and the risks, here are the strategic implications and indicators to watch going forward:

1. Deposit Growth & CASA Mix: A key lever will be how well the bank can continue to grow deposits and improve the proportion of CASA. Weakness here would undermine lending growth capacity or margin.

2. Gradual Normalization of LDR: The bank’s stated aim to bring LDR down to ~85–90% over the next couple of years is wise. Expect them to slow loan growth, securitize, or shift capital into investment securities to manage this.

3. Maintenance (or Improvement) of Margins: In a competitive market, margins will be under pressure. The bank will need to price loans carefully, manage funding costs, and consider hedges or liability restructuring to protect NIM.

4. Stringent Credit Underwriting & Monitoring: As the loan book scales, vigilance is essential. Sectoral exposure limits, stress testing, early warning systems, and tighter collections will become differentiators.

5. Strong Liquidity Management: The bank must keep sufficient high-quality liquid assets (government securities, cash equivalents) so that short-term disruptions do not force distress actions.

6. Cost Discipline & Digital Leverage: To protect the cost-to-income ratio even while growth scales up, automation, process optimization, branch rationalization, and technology investments will be essential.

7. Capital Planning: Growth strategies must be aligned with capital requirements. The bank should plan capital issuance or internal accrual retention so as not to suddenly dilute or hamper growth.

8. Merger Synergies & Operational Integration: Realizing the benefits of the HDFC merger, integrated systems, customer cross-sell, rationalization of overlapping functions, and unified risk controls will be key. Any lag in integration could erode efficiencies.

9. Macroe Sensitivity & Scenario Planning: Given the external environment uncertainties (rate cycles, inflation, global shocks), scenario-based planning should be standard. The bank must have contingency buffers.

10. Transparency & Market Communication: Because external investors and analysts care deeply about asset quality, capital, and funding trends, transparent disclosures will help maintain confidence.

Final Thoughts

The FY 25 balance sheet of HDFC Bank, in its post-merger scale, presents a picture of ambition, strength, and risk. The bank is pushing aggressively to expand its lending footprint, relying strongly on deposits for funding, all while keeping efficiency and margins under control. Its capital buffers are healthy, and asset quality has not yet shown red flags.

But that high loan-to-deposit ratio, reliance on deposit growth, margin sensitivity, and credit risks mean the bank must tread carefully. Execution will matter more than ambition. If HDFC Bank succeeds in gradually normalizing leverage, protecting margins, maintaining credit discipline, and integrating the merged entity efficiently, it will emerge stronger.

Disclaimer:

This article is intended solely for educational and informational purposes. It should not be construed as financial, investment, banking, or trading advice. The analysis is based on publicly available data and company disclosures as of the time of writing, and financial metrics or interpretations may change as new information emerges. We are not registered with SEBI, RBI, IRDAI, or any financial regulatory authority, nor do we offer personalized financial advisory services. Readers should independently verify all information and consult with a qualified financial professional before making any banking, investment, or lending-related decisions.