For many Indian households, fixed deposits have always been the default choice for savings. They feel safe, simple, and predictable. You know how much interest you will earn, you know when the money comes back, and you do not need to watch markets every day.

But 2025 has changed the mood. Interest rates are coming down again, and fresh FD rates are no longer as attractive as they were a year or two ago. This has pushed many savers to ask a serious question: should some money move out of fixed deposits and into bonds?

This article answers that question in full detail. It explains the current rate situation, how bonds work, how they differ from FDs, where risks lie, how retail investors can invest, and how to build a sensible savings mix. The aim is simple: after reading this, you should not feel the need to look elsewhere for clarity.

The interest rate situation in 2025

The starting point of this discussion is interest rates.

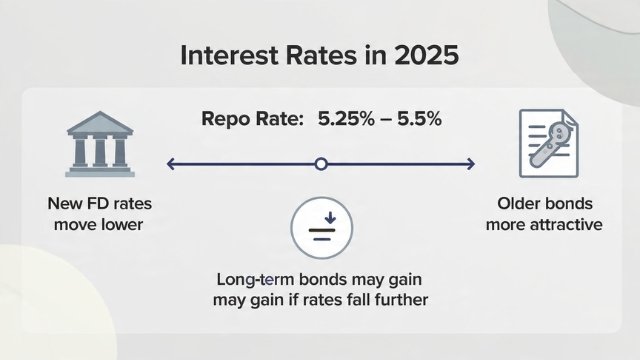

The Reserve Bank of India has reduced the repo rate to around 5.25–5.5 percent in 2025. Inflation has stayed mostly under control, and economic growth has shown signs of slowing. Because of this, the overall policy tone remains supportive rather than tight.

When policy rates fall or stay low, three things usually happen. First, banks reduce the interest they offer on new fixed deposits. Second, existing bonds that were issued at higher rates become more valuable. Third, longer-term bonds may see price gains if rates move down further.

This combination explains why bonds are back in the conversation.

Also Read: The 5 Biggest Investment Questions Young Investors Face

Where fixed deposit rates stand today

As of now, most large public and private banks are offering FD rates in the 6 to 7 percent range for one- to three-year deposits. Senior citizens get a small extra spread, but even that advantage has narrowed compared to earlier periods.

Small finance banks still advertise higher rates, sometimes touching 8.25 to 8.6 percent for specific tenures. These rates look attractive, but they come with limits. Deposit insurance is capped at five lakh rupees per depositor per bank, and smaller banks often rely heavily on deposit growth. This does not make them unsafe by default, but it does mean savers should spread money across banks rather than placing large sums with a single institution.

With policy rates already lower, it is unlikely that FD rates will move meaningfully higher in the near term. If anything, fresh rates may soften further.

What bonds offer in the same environment

Bonds are simply loans that you give to the government or to companies. In return, you receive regular interest payments and your principal back at maturity. What makes bonds different from FDs is that their market price can move up or down before maturity.

There are three main bond categories that matter for most retail investors.

Government bonds are issued by the central government. They are considered among the safest instruments in the country if held until maturity. Current yields vary by maturity but broadly fall between about 5.6 percent and 6.7 percent. Longer maturities pay more, but they also show larger price swings in the interim.

State development loans are issued by state governments. These usually pay more than central government bonds of similar maturity, often by forty to eighty basis points. In 2025, many SDLs offer yields in the 7 to 7.5 percent range. While they are not formally guaranteed by the centre, default risk has historically been very low.

Corporate bonds are issued by companies. These offer higher returns to make up for higher risk. Top-rated corporate bonds in India typically yield between 7 and 8.5 percent. Lower-rated bonds may pay even more, sometimes crossing 9 or 10 percent, but the chance of loss also rises sharply.

Why bonds look tempting when rates fall

When interest rates fall, new FDs pay less. Bonds behave differently. Older bonds with higher coupons become more valuable because they pay better than newly issued ones. This can push bond prices higher in the secondary market.

For someone who holds a bond till maturity, the price movement may not matter much. But for those who may sell earlier, falling rates can lead to capital gains.

This is one reason many investors start looking at bonds when the rate cycle turns downward.

How fixed deposits and bonds really differ

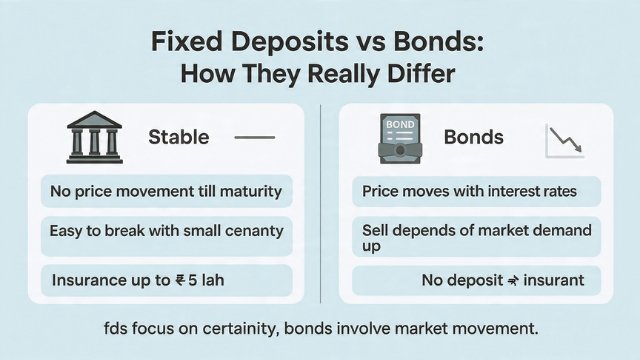

On the surface, both FDs and bonds promise interest and return of principal. In practice, the experience is quite different.

Fixed deposits are straightforward. If you hold them till maturity, there is no price movement. Even if rates rise or fall, your return does not change. Breaking an FD is usually easy, though you may pay a small penalty. Deposits are insured up to five lakh rupees per depositor per bank, which adds comfort for smaller sums.

Bonds, on the other hand, trade in the market. Their prices move when interest rates change. If rates rise, bond prices fall. If rates fall, bond prices rise. This movement is sharper for longer-maturity bonds. Bonds also do not have deposit insurance. If the issuer defaults, investors may lose money.

Liquidity is another difference. While an FD can usually be broken with a click or a branch visit, selling a bond depends on market demand. Sometimes you may not get a fair price, especially for smaller or lower-rated issues.

Also Read: Mutual Fund Trustees Must Lead With Oversight and Integrity, Says SEBI Chairman

The three risks bond investors must understand

Anyone shifting from FDs to bonds should clearly understand three major risks.

The first is credit risk. Government bonds do not carry this risk, but corporate bonds do. If a company faces financial trouble or fails to repay its debt, bondholders can lose both interest and principal. This is why most conservative investors stick to top-rated issuers only.

The second is interest rate risk. Bond prices move opposite to interest rates. If rates rise after you buy a bond, its market value can fall. This matters most if you need to sell before maturity. Longer-term bonds show larger price changes than shorter-term ones.

The third is liquidity risk. Bonds do not always trade easily. In stressed markets or for less popular issues, buyers may be scarce. This can force sellers to accept lower prices. Because of this, bonds work best when you can hold them till maturity.

Direct bonds versus debt mutual funds

Retail investors can access bonds in two main ways: buying bonds directly or investing through debt mutual funds.

Direct bond investment suits those who have larger amounts to invest and are comfortable holding bonds till maturity. Minimum investment sizes are often one to two lakh rupees per bond, and a larger portfolio is needed to spread risk across issuers and maturities. Managing coupon reinvestment is also the investor’s responsibility.

Debt mutual funds pool money from many investors and invest across a range of bonds. This provides instant diversification and professional management. Entry amounts are much lower, and investors can use monthly investment plans to spread timing risk. Funds also handle reinvestment and issuer tracking.

For many small investors, debt funds offer a simpler way to access bond returns without operational complexity.

How bond maturity affects returns and comfort

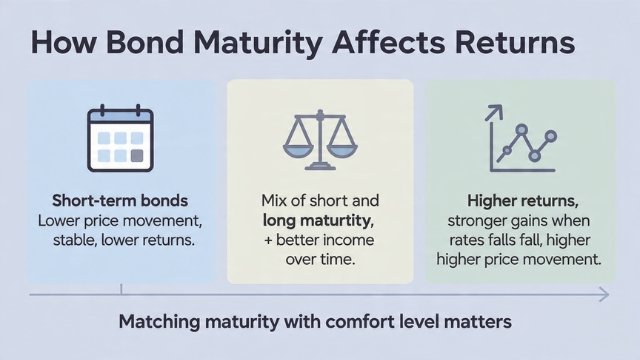

Bond maturity plays a big role in how returns behave.

Short-term bonds tend to be more stable. Their prices do not move sharply when rates change, but their returns are also lower. Long-term bonds pay more and benefit more when rates fall, but they can show sharp price movement along the way.

Many investors choose a mix rather than an extreme position. Shorter maturities provide stability and predictable income, while longer maturities add return support over time. This balance often suits those with long-term goals but limited tolerance for sudden swings.

How retail investors can buy bonds in India

Retail investors now have more access to bonds than in the past.

One route is online bond platforms, which allow investors to browse available bonds, compare yields, and place orders through a demat account. Another route is traditional brokers or wealth advisers, who can help source specific issues and assist with paperwork.

For government bonds and state loans, investors can also use the RBI Retail Direct platform. This allows direct purchase without intermediaries and is aimed at investors seeking pure government-backed safety.

In all cases, a demat account is required, and bonds are held electronically.

Also Read: India’s Economic Growth in 2025

A simple approach to investing in bonds

For someone new to bonds, a clear process helps avoid mistakes.

The first step is ensuring you have a demat and trading account. The second is checking the issuer’s strength, the interest rate offered, and the maturity date. The third is deciding whether to buy a new issue or an existing bond. The fourth is placing the order using the bond’s identification number. Once purchased, the bond sits in your demat account, interest is credited to your bank account, and the principal comes back automatically at maturity.

When moving savings from FDs to bonds makes sense

Shifting some money into bonds makes sense under certain conditions.

If your time horizon is five to ten years or more, bonds can help you lock into better returns than fresh FDs. If you can ignore short-term price movement and are comfortable holding till maturity, government bonds, state loans, and top-rated corporate bonds can fit well. If your aim is steady income rather than daily liquidity, bonds may add value to your savings mix.

When fixed deposits still deserve priority

Despite the appeal of bonds, fixed deposits still play an important role.

FDs are better suited for emergency funds, near-term goals, and money that cannot afford any uncertainty. They are simple, predictable, and easy to access. For goals within three years, safety and ease often matter more than chasing slightly higher returns.

Building a balanced savings structure

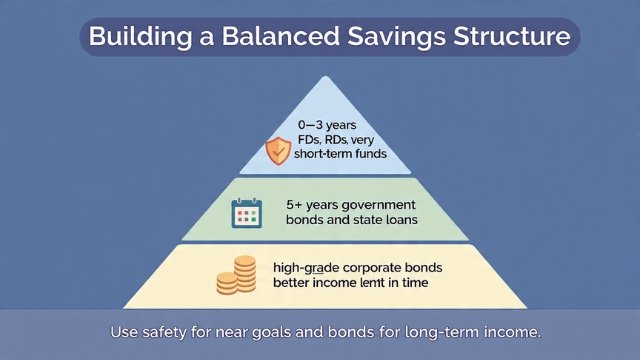

Rather than choosing between FDs and bonds, many investors benefit from using both.

For emergency needs and goals within three years, most money can stay in large-bank FDs, recurring deposits, or very short-term funds. A small portion may be placed in short-maturity government bonds or high-quality debt funds if comfort allows.

For medium and long-term goals, a larger share can move into government bonds, state loans, or high-grade corporate bonds, either directly or through funds. The remaining portion can stay in FDs or be spread across other assets depending on risk comfort.

This layered structure allows safety where it matters and better income where time allows patience.

Also Read: How to Start Algorithmic Trading in India

Return comparison in 2025

The table below gives a broad idea of how different options compare in terms of annual returns. Actual returns can vary based on timing and issuer.

| Investment option | Typical annual return range |

|---|---|

| Large bank fixed deposits | 6% to 7% |

| Small finance bank fixed deposits | 7.5% to 8.6% |

| Government bonds | 5.6% to 6.7% |

| State development loans | 7% to 7.5% |

| AAA corporate bonds | 7% to 8.5% |

| Debt mutual funds | Varies by fund type |

How bonds compare with FDs at similar return levels

For investors comparing options at roughly similar returns, it helps to see differences clearly.

| Feature | Fixed deposits | Bonds |

|---|---|---|

| Safety | High, within insurance limit | Depends on issuer |

| Price movement | None if held | Yes |

| Liquidity | Easy | Market-dependent |

| Entry amount | Low | Higher |

| Management effort | Very low | Medium |

| Return stability | High | Varies |

Final thoughts

Moving savings from fixed deposits to bonds is not about replacing one with the other. It is about using each where it fits best.

In a lower-rate phase like 2025, bonds can help part of your savings earn better income, especially for long-term goals. Fixed deposits continue to serve well for safety, simplicity, and short-term needs.

A calm, balanced mix, chosen with awareness of time horizon and risk comfort, usually works better than extreme choices. If you understand how bonds behave and use them patiently, they can quietly strengthen your overall savings plan without unnecessary stress.